The sales pitch sounds too good to be true, and should instantly set-off financial alarm bells. Here is how I have heard it. Give us your money today and we will guarantee you at least 5%, 6% — and some still promise 7% — for the next 5, 10 or 15 years. And, if-and-when the stock market ever recovers you might earn even more! This, to remind you, is being offered in an economic environment in which Treasury Bill’s yield 0% and Government Bond’s yield barely yield 5%.

And, although most of the promotional material touting “guaranteed lifetime income benefit (GLiB)” variable annuity (VA) products are very careful to emphasize that the guaranteed rate is applied to a base and not to the account value itself, I can attest that few people understand how to convert the 7% number into a rate that is comparable to interest in a bank account or investment returns on a mutual fund. The marketing material is speaking the language of investment Celsius to human beings that are hard-wired to understand economic Fahrenheit.

So, to clear this up I would like to devote the inaugural article of ANNUITY ANALYTICS to explain the arithmetic, correctly. Say you are 55 years-old and invest $100,000 in a variable annuity (VA) policy that offers a minimum 7% guaranteed growth rate. This implies that at the very least you will have an income base of $196,715 by the age of 65. This number is computed in a straightforward manner by multiplying $100,000 times (1.07)^10. Of course, the income base might be even higher if the underlying investment subaccounts cooperate – by defying recession’s gravity and all management fees – and rise by even more than 7%. The contract further stipulates that the income base – whatever it is at the withdrawal commencement date, say age 65 – will be multiplied by a guaranteed withdrawal rate, say 5%, to determine your lifetime income benefit. I will refer to these two critical numbers as the guaranteed growth rate (i.e. 7%) factor and the guaranteed withdrawal (5%) factor. Every VA policy with a GLiB includes both sets of numbers. Obviously, the larger the number the better it is for the consumer.

So, just to recap, if you want to retire at 65, the absolutely worst case scenario – and we seem to be experiencing a lot of those lately – is a guaranteed lifetime income of 5% times the $196,715 base which is approximately $9,836 per year for life. Remember this number. It sounds nice, but it is precisely where my problems start.

Did you ever wonder, what does it cost to purchase a pure lifetime pension at the age of 65, one that pays the same $9,836 per year for life? This is not a hypothetical question. There is an active market for income annuities, and they have been sold by major insurance companies for hundreds of years. In March 2009 the cost of a $9,836 per year of lifetime income, starting immediately at the age of 65, was approximately $122,940. This number is actually an average from a number of competitive insurance vendors and some will charge you less (in exchange for taking on some insurance company credit risk.)

But as you probably noticed, $122,940 purchase price for the same income stream is around 38% less than the guaranteed base of $196,715.

In other words, to get the enticing growth rate factor (7%) applied to the base, you have to put-up with a very distasteful withdrawal rate factor (5%). The 7% growth can’t be disentangled from the 5% withdrawal rate. If you accept one you have to take the other. It’s like going to your favorite store’s sale in which everything is 50% off, but the local sales tax has been simultaneously increased from 5% to 100%. The 50% discount feels good for the few minutes it takes you to walk from the display shelf to the cash register. Once you check-out you will realize that your left-hand has pick-pocketed your right wallet.

In my opinion, the correct way to translate the growth factor (7%) and the income factor (5%) into a proper and comparable investment return is a three step process, which behooves all financial advisors understand and to explain to their clients.

First, get an immediate annuity income quote – with no guarantees or survivor benefits – for a $100,000 premium and a purchase age of 65, or whenever you plan to start the income. Divide the annual income into this $100,000 premium. That is what we call the annuity factor. Step two. Multiply the worst case scenario guaranteed income by the annuity factor at age 65 (or whenever you plan to start the income.) In the above case the annuity factor was 12.5, which leads to the mentioned value of $122,940. Then, finally, divide this number by the original $100,000 premium and solve for the implied growth rate over the 10 year waiting period. This is (122940/100000)^(1/10)-1, whose value I’ll get to in a minute. In other words, compute the annual investment return that makes $100,000 become $122,940 after ten years. Once again, the $122,940 is the cost of buying $9,836 for life at age 65.

Here is the bottom line. In the (7%, 5%) guarantee pairing, the number works out to a meager 2.0%. That is the true value of the growth & withdrawal rate combinations. That is a number in units of that are directly comparable to bank interest, mutual fund returns and T.Bill yields.

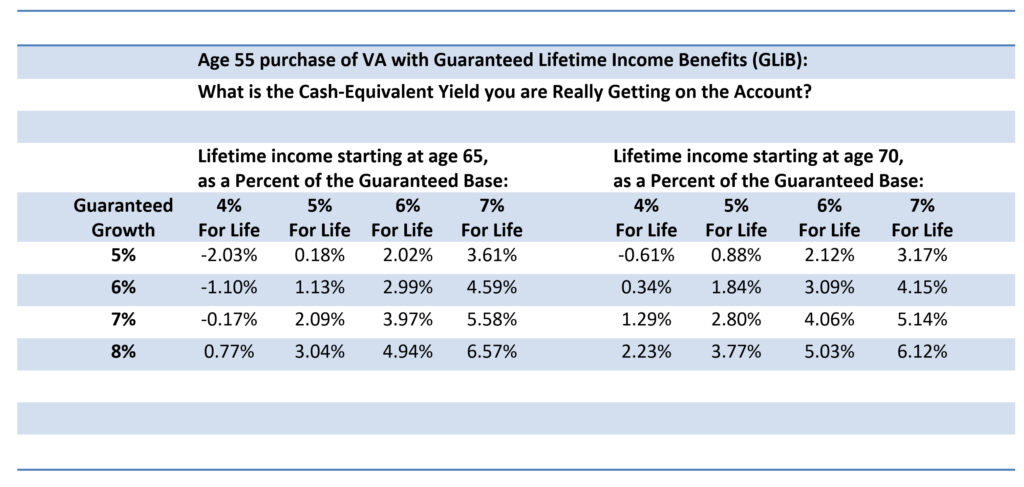

Different ages, waiting periods and guaranteed growth and withdrawal rate combinations will lead to a variety of implied investment returns, but they inevitably always work out to less than the growth rate highlighted in the policy. The following table displays a number of other common combinations.

For example, a VA+GLiB purchased at age 55, that promises a 5% bonus and a 5% lifetime income starting in 15 years, at age 70, is equivalent to a 0.88% equivalent yield. If the guaranteed growth is 5% but lifetime income is 6%, the equivalent yield is 2.12%. The 7% for life would equal 3.17%, etc.

Now, don’t get me wrong here. As many practitioners know, I have been observing, researching and commenting on this industry for many years. There is probably no greater (academic) advocate of the importance of hedging personal longevity risk, individual inflation and the terrifying sequence of returns. I have given credit where it’s due, advocated where appropriate and criticized where necessary.

I now worry that consumers will rush into the jaws of inappropriate sales because they misunderstand and hence do not know how to properly translate Celsius digits into Fahrenheit interest.

In fact, my preferred way of explaining or interpreting the guarantees with a variable annuity policy is by conceptually splitting the product in two. The first is a straightforward investment and the other component is the embedded equity put option (a.k.a. downside protection). The put option guarantees that if markets decline the contract can be converted or exchanged into a lifetime income vehicle. Moreover, every put option has a strike price and the strike price of the VA+GLiB combintation is the amount it would cost you or your client to purchase an equivalent income stream in the open market.

For example, under a 7% guaranteed growth rate and 5% of lifetime income, the fair market cost at the age of 55, of a $9,836 per year income stream starting at age 65, is $71,500 TODAY. This is the price of a pure deferred annuity (a.k.a. ALDA) with a ten year waiting period. In my mind, the VA+GLiB is $100,000 invested in a diversified portfolio with a put option that is struck at $71,500 and is currently 28.5% out of the money. The value of this put option and the embedded protection depends primarily on the volatility of the underlying subaccounts. The more equity in the subaccounts, the more valuable is the put option. Likewise, the greater the asset allocation restrictions, the less valuable is the put. The is basic derivative economics. Indeed, that is the correct value proposition of the VA + GLiB.

In sum, it’s time to acknowledge that 7% is really closer to 1% and 6% is pretty much zero. Remember, allocating a portion of your nest egg to a variable annuity with a guarantee can be an excellent strategy, but make sure it’s for the right reasons.

(This is a longer version of a condensed article that appeared on ThinkAdvisor.)