The “A” word strikes fear into the hearts and wallets of advisors throughout the financial services industry. Irreversibly handing over a lump sum of money — to an insurance company, no less — in exchange for a promise to slowly return this money over a very long period of time rightfully feels like financial suicide to many retirees.

Ironically, the loathed process of annuitization is at the core of Defined Benefit (D.B.) pensions – a steady generator of retirement income, which is cherished by retired civil servants around the world – and helps mitigate longevity risk, something I discussed in last month’s lesson. In fact, the lifetime income guarantee from Social Security is also based on the annuitization process. You can’t securitize, cash-in or monetize your income stream, although it definitely lasts for the rest of your life.

So which one is it then? Is voluntary annuitization to be shunned and avoided or is it the foundation of a well balanced retirement income plan? In this month’s lesson I will provide a closer look at the pros, the cons and some of the fixes. Indeed, if you are going to accept annuitization as a partial solution for your client’s retirement income, then you should understand the mechanics of how and when is works. Likewise, if you plan to bypass them as viable solutions, it makes sense to talk intelligently about their shortcomings.

The Pros:

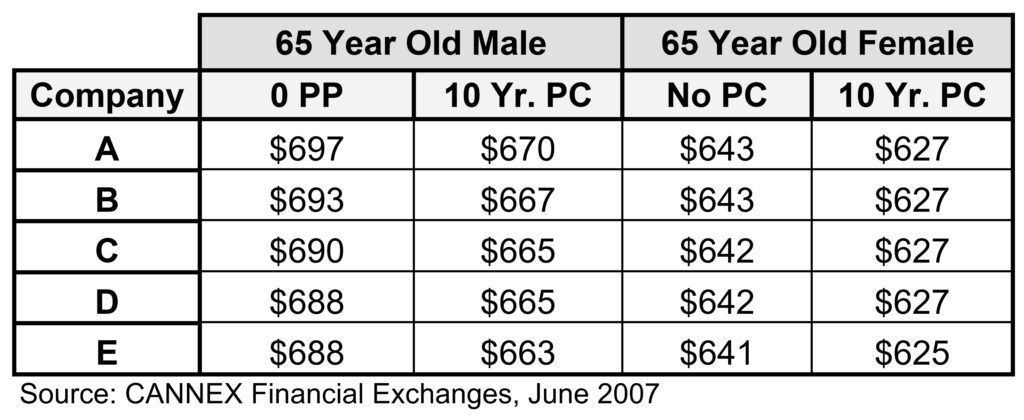

Table #1 displays sample quotes for single premium immediate annuities (SPIAs) in mid-June 2007. Each column contains the top five quotes from five different insurance companies for a given purchase age and gender. These numbers are provided by an intermediary called CANNEX Financial Exchanges which is attempting to provide the equivalent of a stock exchange quoting-system for retirement income products; more on that later.

Table: What Does a $100,000 Buy You?

Monthly Income for Life

Here is how to read these numbers. For example, if you or your 65 year-old female client invests or deposits $100,000 in a SPIA, then the best insurance companies offer a range of $643 to $641 per month for life; pre-tax of course. Note that this income stream will completely cease upon death. Indeed, if she dies ten, five or even one year into the annuitization period, everything is lost.

Naturally, most if not all people select a guarantee period for their SPIA, at the expense of a slightly lower income stream. For example, as shown in the table, if your 65 year-old client selects a 10-year payment certain (PC, as they are often called), the income is now lower; the top company range is $627 to $625 per month. A 65 year-old male gets slightly more. His numbers range from $670 to $663 if he selects a 10 year period certain and $697 to $688 if he does not. They offer $25 to $30 less per month, if you want assure at least 10 years of payments (to someone).

On a slightly more technical level, if you divide the annual income generated by the basic SPIA, by the initial premium of $100,000 you arrive at what I call the annuity yield. For example, using payouts from the table at age 65 — with zero years of certain payments – the best company yields range from 8.36% to 8.26% for males and 7.71% to 7.69% for females.

These numbers have remained steady at these levels over the last 2-3 years, but longer term they have been declining as a result of both historically low interest rates as well as increasing longevity. As people are projected to live longer, the insurance company can’t offer as much.

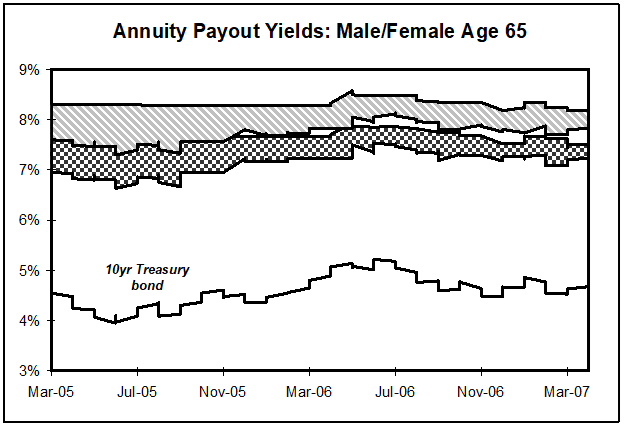

The figure illustrates the weekly evolution of annuity yields over the last two years. I have plotted the best/worst annuity yields – for both males and female — offered by insurance companies in the U.S. – that are part of the CANNEX system — in comparison to the yield on a 10-year Government bond.

Figure #1

There are a number of important insights to be gleaned from this chart. First, notice that the yield – which is the annualized income stream divided by the initial premium – is much greater than the yield on a government bond. The reason for this is because your lifetime income is an integrated blend of three distinct cash flows. First you are getting a type of interest coupon on your money; second you are getting a portion of your premium back, and third you are getting a portion of other people’s money. In fact, for this reason it’s a bit of an apples-and-oranges situation to compare the unique yield of a life annuity to any fixed income instrument.

The insurance actuaries try to forecast approximately how many people will die in any given year – and they take into account the risk of getting this calculation wrong – and then give the annuitant a “longevity credit” based on this estimate. Of course, all of this alchemy takes places behind dark curtains since the annuitant receives a constant periodic check that blends all of these varying components.

Notice also another subtle fact. The spread between the highest/lowest quotes, i.e. what the most competitive versus least competitive insurance company is offering appears to be shrinking over time. In other words, the gains from shopping or the dispersion between companies is on the decline. The decline reflects a market that is becoming more commoditized and more competitive. And, although insurance companies might not welcome this trend, the end-user can only benefit. In fact, the availability of various annuity quoting websites — and the CANNEX Financial Exchange which provides a transparent platform for users to see quotes in real time — helps accelerate this trend. Interestingly, in the Canadian SPIA market – for which more extensive historical payout data exists – the declining trend is quite clear.

Back to our discussion of annuity pros, SPIAs and their financial cousins, provide lifetime income that can not be outlived. They also provide a mechanism for pooling, sharing and hedging longevity risk over a large population, which leads to a higher yield for surviving annuitants. Finally, they provide stable and predictable income that is not subject to the vagaries of the stock market. It’s a fixed income product together with a longevity coupon “kicker”. Its important to remember that if you die prior to reaching a financial break-even point, the insurance company doesn’t keep the money – rather, it goes to subsidize payments for those who exceed the averages.

The Cons:

There are a number of legitimate criticisms that are often leveled against SPIAs and other annuitization-based products. One of the major concerns is the almost complete irreversibility of the decision once the policy has been funded and the product starts generating lifetime income. Unlike almost any other financial instrument – like a stock, bond, mutual fund or ETF — one can not redeem, cash-in or even sell a SPIA in the secondary market.

But, although this irreversibility is frustrating, it is perfectly understandable and economically justifiable. Imagine what would happen if individuals who are in poor health, or perhaps even on their death bed, were allowed to “return” their SPIA certificate to the insurance company and ask for a refund netted against the payments they had already received. Obviously, everyone would do this at some point in their life and the insurance company would completely lose their ability to diversify longevity risk across a large pool of annuitants. This is often called adverse or anti-selection and is one of the great justifiable fears for insurance actuaries. Remember, the reason you and your client are getting the yield above and beyond what is available in the fixed-income bond market is because the insurance company can internally shift and subsidize longevity.

Now, some companies have responded to the lack of liquidity concern by offering cleverly engineered SPIAs that provide partial-liquidity, refunds and death benefits. And although these solutions might alleviate retirees’ concerns about annuitization, they come at the expense of the above mentioned longevity credits. You can’t have your longevity insurance cake, and eat it too. Just like with car, health and life insurance, if a company offers you a policy in which you get some of your premiums back if you don’t put in a claim – the premiums you pay will be much higher. There is no free lunch and from a practical perspective I would recommend buying less of a “pure” SPIA than more of a “loaded” one.

A second concern is inflation. This is a topic I tackled in a lesson a few months ago. Remember that most currently-sold SPIA products provide nominal payments that decay in real terms over time. The purchasing power of that income may decline by more than 60% by the time you are half-way through your retirement. Of course, you can purchase inflation-linked or cost of living adjusted (COLA) life annuities, but the price you pay is in the form of greatly reduced up-front payments. In fact, the pure inflation-linked annuity market is not as competitive as the much larger nominal SPIA market, nor is it clear that it better hedges retiree inflation either.

A third quite legitimate concern is credit risk or the possibility the insurance company defaults at some point in the distant. Right now the best rated insurance company in the U.S. offering SPIA product is a Aa1 according to Moody’s Investor Services, while the lowest in our sample was rated A1. Many buyers are concerned about the possibility of downgrades and eventual defaults over these long horizons. On the other hand, it is however important to remember that there are State guarantee funds that are meant to protect the policyholder in the event of default, up to certain limits. Also, insurance company defaults or insolvencies are quite rare. Nevertheless, the concern is there. In fact, one of the reason some insurance companies pay/offer less to their annuitants is precisely because their credit rating is better. You are getting a reduced income, but one that is more secure. Either way, one easy solution would be to diversify across companies and hence reduce some concerns by spreading credit risk across issuers. It might cost a bit more in time and effort up-front, but could be worth the piece of mind.

The Fixes:

So, what can you and the insurance industry do to help promote annuitization, above and beyond some of the minor tweaks I mentioned earlier?

First, I continue to believe that for purely psychological reasons if nothing less, people will continue to shun the idea of irreversibly locking-up a large portion of their life savings at one point in time. This is especially true if they have not been conditioned to do so in the lead-up to retirement. The best way to position annuitization is as a gradual default strategy, which is effectively how one accrues credits in a Defined Benefit (DB) pension. Thus, the optimal strategy might be to annuitize a few thousand dollars at the age of 65, then a few thousand more at 70, and a few more at 75, etc. Today’s contracts – let alone advisor compensation – might not be geared towards this process, but I foresee it will happen soon.

Another solution to the annuitization dilemma, is to offer the implicit longevity insurance they provide as an attachment or rider on traditional investment products that consumers are more comfortable and familiar with. These riders can then be positioned as worst-case-scenario protection if all else goes wrong with the underlying investments. In fact, the industry is having great success with this approach which is implicit within guaranteed minimum income benefits (GMIBs) and guaranteed minimum withdrawal benefits for life (GMWBfL), which are attached to variable annuity policies. Sure, your client might not want to annuitize today, but it can serve as a fall back strategy.

Other innovations – which might not be so innovative within a historical context – involve repackaging variable (as opposed to fixed) immediate annuities so that their income stream does not fluctuate as much. And, although the sale of these products is on a steady decline, they actually make the most sense to me. They provide mortality credits plus the ability to gain the equity risk premium.

The final step — once you accept the benefits of having some level of lifetime income that can not be outlived — is the overall portfolio’s optimal allocation to this product class. How much of your retirement income should emanate from SPIAs versus a systematic withdrawal plan (SWiP) and/or variable annuity with a guaranteed living benefit (GLB). And, while on the topic, at what age should you acquire these types of longevity insurance? As you can imagine, this is a topic for another lecture. Stay tuned.

(This is a longer version of a condensed article that appeared on ThinkAdvisor.)